December Newsletter: BTC Teeters on the edge, Monad launches, Ethereum ships Fusaka and More.

- Ameer Omar

- Dec 8, 2025

- 6 min read

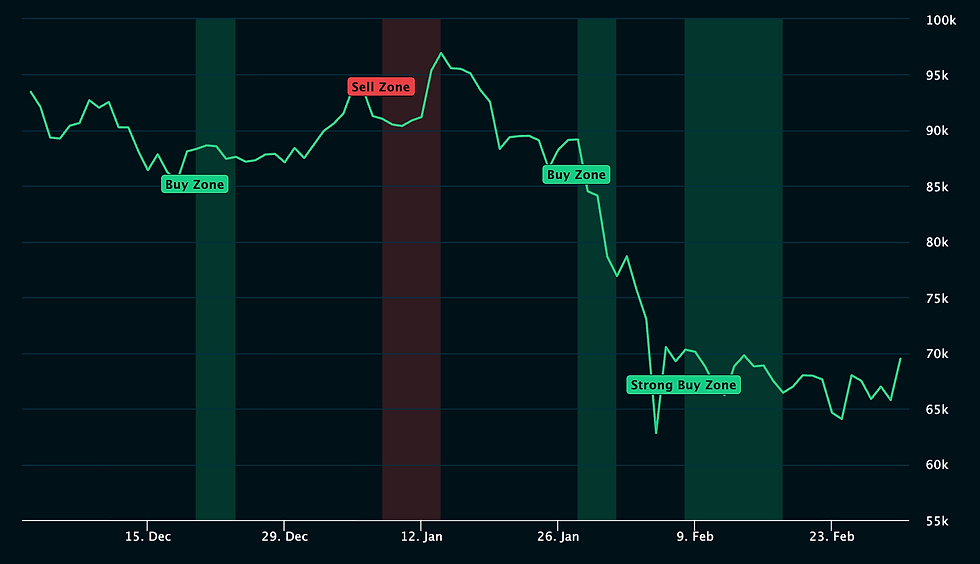

November 2025: The Month Markets Lost the Plot

Nothing about November behaved as a “bull market year” is supposed to. Bitcoin and Ethereum delivered their worst November since the FTX collapse. China banned crypto again and, somehow, markets acted surprised. Japan revived the yen-carry unwind that crushed traders in mid-2024. A fresh round of geopolitical rumors clouded the macro picture. And yet, pockets of real progress across Ethereum, Bitcoin, Solana, BNB Chain, and the broader security stack quietly pushed the industry forward.

The market traded as if everyone expected pain, yet the setup suggested the opposite. This strange tension defined the month.

Japan Reopens the Pressure Valve

The most important macro story was, again, Japan. Two-year JGBs climbed toward 1 percent, and ten-year yields approached 1.9 percent, both the highest since 2008. Overnight Interest Swaps priced in strong odds that the BOJ would hike in December. Every time this happens, yen-funded carry trades wobble.

The mechanics haven’t changed. Global macro funds borrow in yen or short JGBs, then park the proceeds in higher-yielding USD and EUR assets. When Japanese rates rise, the funding leg becomes unstable. Everyone races to unwind. High beta positions get thrown out first, and crypto sits on that chopping block. When the BOJ moved in 2024, BTC fell nearly 30 percent as macro books de-risked. November echoed that playbook with BTC shadowing the Nikkei lower during Asia hours.

The BIS has warned that most yen borrowing does not appear on traditional balance sheets. Roughly $14 trillion in FX swaps and forwards have JPY on one side, backed by only $271 billion in visible loans. Non-bank allocators provide much of the liquidity and tend to pull back quickly when volatility rises. That feedback loop resurfaced this month.

China helped fuel risk aversion. The PBoC reiterated that all virtual currency activity remains illegal and placed stablecoins in the same category as capital flight tools. Hong Kong crypto equities dropped sharply. The announcement wasn’t new, but the market reaction showed how nervous investors were.

A Bull Market That Doesn’t Feel Like One

BTC was on track for its worst November since 2022. ETH was on track for its worst since 2018. When you have to compare 2025 to the FTX lows to find a similar stretch, sentiment is already shaky.

The broader narrative became a duel between two ideas. One camp believed the market would carve out a lower high and roll over. Another argued the market was so oversold that any catalyst could produce a sharp rebound. Liquidation heatmaps reinforced the tension. There were more leveraged traders positioned to be liquidated on a move up than a move down, which created a strange paradox. The bullish outcome could hurt more people than the bearish one.

Markets punish crowded trades. Nobody agreed on which scenario was more crowded.

Two counter-signals caught attention. Monad listed MON on exchanges after months of delaying its launch, which many interpreted as a vote of confidence in December’s outlook. And Coinbase hinted at sizable product announcements scheduled for December. Exchanges tend to launch new initiatives into strengthening, not weakening, markets. The caveat is that this logic has also failed near the top.

Macro clouds added to the uncertainty. Expectations for the Fed to dial back QT, hopes for progress in Ukraine, and the possibility of tariffs being struck down looked constructive. On the other hand, reports surfaced that the US might escalate operations in Venezuela. With that mixture, December looked primed for volatility on both sides.

Bitcoin Marks a Milestone in Security

In a month defined by discomfort, Bitcoin delivered one of its most mature moments yet. Quarkslab, funded by Brink and coordinated by OSTIF, completed the first third-party security audit of Bitcoin Core. The team spent 100 person-days examining core modules such as the P2P layer, mempool, chain management, and consensus code.

There were no high or medium-risk findings. Only two low-risk issues and a small set of improvement suggestions. For a system that secures trillions of dollars in value, the audit marks a meaningful step toward more formal, rigorous software governance.

Ethereum Moves Toward Real Scale

Ethereum’s roadmap advanced on multiple fronts.

Fusaka Upgrade Testnets were completed, and mainnet activation was scheduled for early December. Fusaka introduces PeerDAS, which lets validators verify data availability with small random samples rather than downloading full blobs. This cuts bandwidth needs by roughly 85 percent and ensures home stakers can continue participating as data throughput grows. Coupled with a gas limit increase to 60M, Ethereum set the stage for higher throughput and stronger support for rollups.

Glamsterdam Prep Developers aligned around ePBS for the consensus layer and Block-Level Access Lists for the execution layer. Some anti-censorship tooling may be pushed to a future upgrade, but only after a credible commitment.

Privacy and Cross-Rollup UX Vitalik introduced Kohaku, a new privacy framework that aims to make opt-in private transactions standard for wallets. Ethereum teams also proposed an Interoperability Layer built on account abstraction, allowing users to execute actions across multiple L2s directly from their wallet without bridges or relayers.

Ethereum L2s Hit the Acceleration Phase

ZKsync launched the Atlas upgrade with 1-second ZK finality and 15,000+ TPS. Atlas treats Ethereum as a real-time settlement hub and enables ZKsync-based chains to tap Ethereum liquidity without running separate pools.

ZKsync’s Airbender prover demonstrated that full L1 block proofs can be generated with only two RTX 5090 GPUs. Vitalik viewed it as a major milestone but warned that worst-case block proving remains the real constraint.

StarkWare rolled out S-two, its new proving system, which now validates every Starknet block and supports decentralized and client-side proving.

Solana, BNB Chain, and Avalanche Press Forward

Solana introduced a proposal to double the rate of inflation reduction. The change would move SOL toward its long-term issuance target nearly three years faster and reduce issuance by about 22 million SOL over six years. Community debate was active, but the proposal was viewed as clear and predictable.

BNB Chain released the Fermi hardfork. Block intervals moved from 750 ms to 450 ms, a meaningful boost for throughput. The network also announced the retirement of its multisig service, instructing users to migrate their assets to Safe Global.

Avalanche shipped the Granite upgrade with a target of two-second settlement, lower cross-chain costs, and biometric signature support.

Security Incidents and Market Infrastructure

Cardano suffered a temporary chain split caused by an old-code vulnerability triggered by a malformed delegation transaction. Stake pool operators patched their nodes, and the network re-merged. The episode raised questions about readiness and operational depth across smaller ecosystems.

Upbit was hacked for roughly $32M, with the Lazarus Group suspected. Japan moved toward requiring exchanges to carry reserves to cover hacks. S&P cut Tether’s stability score to “weak,” reigniting debate over stablecoin transparency.

Regulators also made moves. The CFTC approved Polymarket to operate legally in the US, while Nevada blocked Kalshi’s attempt to offer sports betting. Robinhood is prepared to launch its own derivatives and prediction market. Commissioner Pham began recruiting CEOs for an innovation council to formalize engagement between platforms and regulators.

Monad: A Case Study in “Low Float, High Drama”

Few launches generated as much attention this month as Monad.

The airdrop surprised many. Only 3.33 percent of the total supply was distributed to early users. Roughly 76,000 wallets qualified, with an average claim value of $1,380. That put the total airdrop around $105 million at launch, far below HYPE’s billion-dollar distribution in October.

About 60 percent of airdrop recipients sold their allocation, while nearly a third held everything. The big wallets partially exited, which removed much of the early sell pressure. MON briefly dipped below its ICO price before rallying nearly 130 percent in the first two days. With only 10 percent of supply liquid and a $4 billion FDV, traders viewed MON as a “cheap relative” to other L1 tokens. That perception, combined with Coinbase’s new token sale platform, supports near-term price resilience.

On-chain activity surged. TVL doubled from $73 million to roughly $150 million in the first week. Daily active users hovered around 120,000 and transactions averaged about 3 million per day, driven largely by memecoin trading. The speculative rush faded as quickly as it arrived. Funds bridged in during launch left the ecosystem just as fast, and the early memecoins burned out almost immediately.

The longer-term story is different. Monad has reserved nearly 40 percent of the MON supply for ecosystem development, and early user incentives could support the next wave of activity. The directory and discovery layer made it easier for newcomers to find apps, while launchpads like Nad.fun and consumer-focused projects held early attention.

Closing Thought

November was messy, contradictory, and far more interesting than the price charts suggest. Macro fundamentals swung sharply. Crypto traded with a sense of exhaustion. Yet the underlying technology stack grew stronger, faster, and more aligned with long-term adoption.

The tension between fear and progress set the stage for a December where volatility seems inevitable. Whether that turns into a rally or another flush is the wrong question. What matters is that the foundations being laid now will shape the next cycle long after this month’s anxiety fades.

Comments